Piotr Biernacki appointed as member of EFRAG SR TEG

Piotr Biernacki, ESG Reporting Partner at MATERIALITY, has been appointed as member of Sustainability Reporting Technical Expert Group (SR TEG).

Piotr Biernacki, ESG Reporting Partner at MATERIALITY, has been appointed as member of Sustainability Reporting Technical Expert Group (SR TEG).

Soon all large and some small and medium-sized enterprises will report sustainable development issues in accordance with the provisions of the CSRD directive.

On February 23, 2022, the European Commission announced a draft Directive on due diligence in the field of sustainable business development!

We are proud to announce that the commitment of our client – the CCC Group…

On January 20, 2022, draft basic standards for reporting on sustainable development issues were published.

On December 20, 2021, the European Commission published the first set of official responses to the Taxonomy questions.

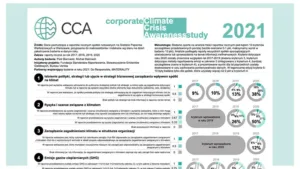

Are Polish companies climate-conscious? What are the priority management actions in the field of climate change?

Two delegated acts supplementing Regulation 2020/852 have been published in the Official Journal of the European Union.

The results of the first Climate Strategy Benchmark implemented by the UNEP / GRID-Warsaw Center…

We are very pleased with the success of the CCC Group for receiving the award for…

Congratulations to our client LUG S.A. on winning the main award in the category of companies listed on the NewConnect market

On September 15, 2021, the results of the CCA – Companies Climate Awareness Survey were announced.

We are proud to announce that Justyna Biernacka, Sustainability Managing Partner at MATERIALITY has been awarded…

On 21 April 2021, the European Commission adopted a package of measures related to implementing sustainable finance.

As part of the sustainable finance package approved on 21 April 2021, the European Commission announced a proposal of Corporate Sustainable Reporting Directive.

In the next two years, we will witness a fundamental change in corporate reporting. It will be implemented through a revision…

On February 20, 2020, the European Commission announced consultations on planned amendments…

A transcription of a discussion from the Polish Association of Listed Companies conference on ESG reporting and sustainable…

A week ago, I described best practice for climate reporting. Now it is worth to describe what changes …

If you are still wondering how to best report on issues related to climate or what you can learn from such reports, look no further.

A sustainable development strategy is a tool which complements a company’s business strategy with ESG …