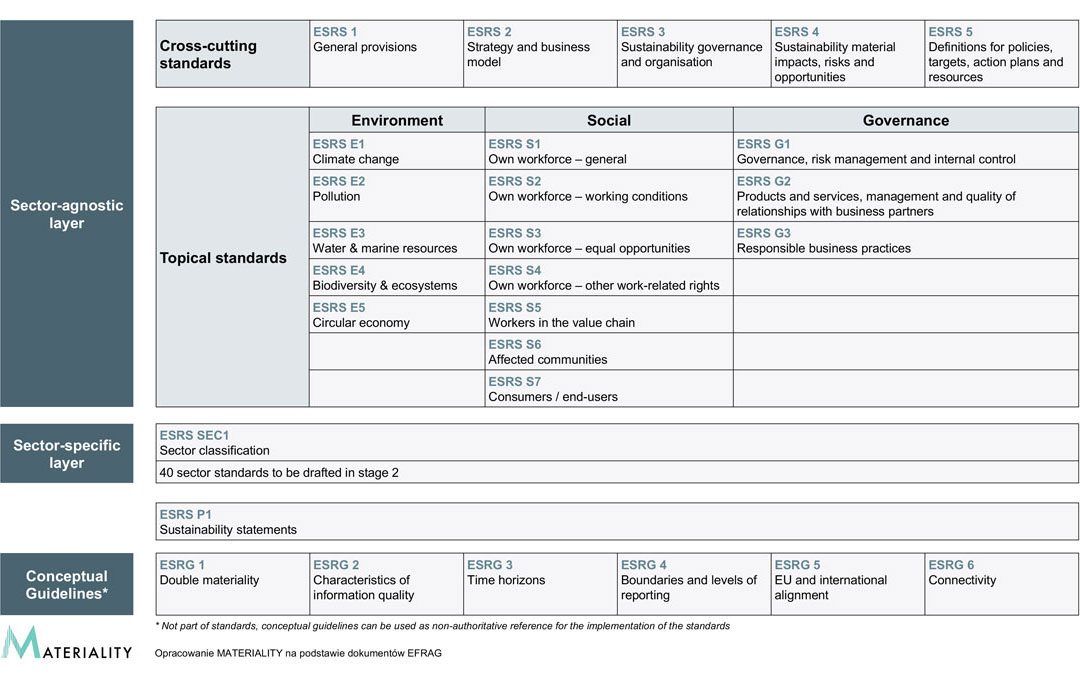

Topical standards: Environment

ESRS E1 Climate change [plik]

ESRS E2 Pollution [plik]

ESRS E3 Water and marine resources [plik]

ESRS E4 Biodiversity and ecosystems [plik]

ESRS E5 Circular economy [plik]

Topical standards: Social

ESRS S1 Own workforce – general [plik]

ESRS S2 Own workforce – working conditions [plik]

ESRS S3 Own workforce – equal opportunities [plik]

ESRS S4 Own workforce – other work-related rights [plik]

ESRS S5 Workers in the value chain [plik]

ESRS S6 Affected communities [plik]

ESRS S7 Consumers and end-users [plik]

Topical standards: Governance

ESRS G1 Governance, risk management and internal control [plik]

ESRS G2 Products and services management and quality of relationships with business partners WP [plik]

ESRS G3 Business conduct [plik]

Sector specific standards

ESRS SEC1 Sector classification standard [plik]

Presentation

ESRS P1 Sustainability statements [plik]